The Airports Council International (ACI) Asia-Pacific’s latest Airport Industry Outlook revealed that airfares in Asia-Pacific and the Middle East surged as nations emerged from pandemic-related restrictions.

The fourth edition of the Airport Industry Outlook, developed in partnership with Mott MacDonald, provides an analysis of airfare trends during the pandemic and in the recovery phase, and summarises the 2022 year-end performance of the airport industry in terms of traffic recovery and economics.

The airfares in Asia-Pacific and Middle East were above the global average – up 53% (nominal terms) or 35% (real terms) in 2022 vs 2019, although fares were trending down towards the end of the year as traffic recovers.

Commenting on the surge in airfares, Stefano Baronci, director general, ACI Asia-Pacific, said: “Despite a consolidated recovery of domestic traffic as compared to 2019 levels, and a progressive improvement of international traffic, with peak performances in Middle East and South Asia, the financial health of airport operators continued to be in distress, with 10 consecutive quarters in the red both in terms of EBITDA (earnings before interest, taxes, depreciation and amortisation) and net profit margin.

“Despite substantial efforts by airports to freeze or lower airport charges in 2022, the average 53% increase in airfares throughout 2022, compared to 2019, reveals a fundamental imbalance in the financial stability of the industry as well as pose a threat to the sector’s full recovery in 2023. Fuel prices, wage inflation, insufficient seat capacity relative to demand and a lack of airline competition on specific routes, are the major determinants in the increase in airfares.”

The increase in airfares were significantly above the global average with airline yields (revenue per RPK) that were 29% higher in 2022 than in 2019 in nominal terms. This is in sharp contrast to the financial health of airports, which are still losing money, with regional EBITDA and net profit margins being negative for the tenth consecutive quarter since 2020.

Airfares have increased across sector distances and the different markets served in the Asia-Pacific and the Middle East regions. Airfares in 2022 were much more volatile than in 2019 (pre-pandemic). The largest increases in percentage and absolute terms were reported in areas which applied stringent and long-lasting Covid-19-related travel restrictions, including the Emerging East Asia (mainly China) where yields increased 90% in 2022 over 2019 levels to US$0.21 per RPK, followed by Developed East Asia with yields up 67%. All other regions, including Oceania (+49%), South-east Asia (+35%), the Middle East (+30%) and South Asia (+19%), reported fare increases compared with 2019, despite generally lower than in 2021 as travel restrictions were progressively lifted.

To understand the market dynamics of air fares in more detail, the world’s Top 15 busiest international routes in 2019 were analysed in detail. All but one of these routes are in the Asia-Pacific and the Middle East region – the exception being London Heathrow (LHR) to New York JFK (JFK). Across these busiest routes in 2022, the number of passengers was down 66% and the average airfare was up 77%.

Airfare increases were mainly driven by variations in airline operating costs – such as fuel price and wage inflation – reduced seat capacity relative to demand; less airline competition on some routes; efforts to recover losses incurred during the pandemic and increased debt and interest rates.

Top international routes

The largest airfare increase was reported on routes with strict travel restrictions and scarce frequencies and airlines competition, such as the ones connecting Hong Kong with Manila and Shanghai. Conversely, LHR-JFK passengers had already recovered to 89% of 2019 levels in July 2019 and the airfare increase was a more modest increase of 21%.

Drivers of airline cost

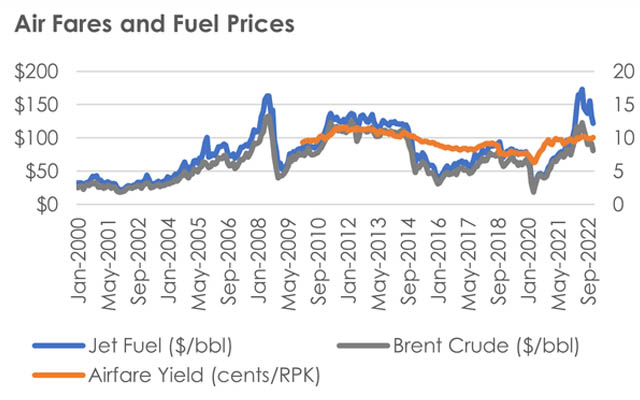

Fuel price is a major driver of airline costs and air fares. Fuel accounts for around one-quarter of airline expenditures on average, and this proportion is larger for longhaul carriers. In recent years, fuel costs have been unusually variable. Jet fuel was 41% cheaper in 2020 compared to the 2019 average price, but 79% higher in 2022 due to oil supply restrictions caused by Russian sanctions and increasing air travel demand.

From the air transport ecosystem perspective, elevated airfares represent a downside factor for full recovery as these may suppress demand and therefore reduce the number of passengers. Airports, on the other hand, need to get back to pre-pandemic traffic volumes in order to restore their economic equilibrium after a prolonged period of operating in the red.

Financial health of airports

Regional EBITDA margin and net profit margins improved significantly in 3Q2022 compared to 2Q2022, thanks to higher airport revenues than in the previous quarters and well contained cost increases due to the growth in passenger demand.

However, the EBITDA margin and net profit remained negative for the tenth consecutive quarter. In terms of total airport revenue, the majority of the sampled airports performed significantly better than in 3Q2021, and on average 65% better than 2Q2022. However, the opening up of major cities from lockdown in China improved air traffic, resulting in a gradual improvement of revenues.