Six parties come together to sign the agreement to jointly promote Busan-Singapore trade and tourism

A six-party MoU has been signed to promote trade, business and tourism flows between Singapore and Busan.

The one-year partnership was signed between Changi Airport Group, Busan Metropolitan City (BMC), Korea Airports Corporation (KAC), Eastar Jet, Jeju Air and SilkAir.

Six parties come together to sign the agreement to jointly promote Busan-Singapore trade and tourism

This follows the allocation of traffic rights to South Korean airlines Eastar Jet and Jeju Air, as well as SilkAir, the regional wing of Singapore Airlines, to operate flights on the Singapore-Busan route.

SilkAir’s four-times weekly service to Busan started on May 1, 2019 while Jeju Air will commence its service to Singapore on July 4, 2019. Eastar Jet is expected to connect the cities in the coming months.

The six-party collaboration aims to strengthen air connectivity between Singapore and Busan and raise awareness of the respective airlines’ product offerings.

In the coming year, residents and travellers from both cities can expect various on-ground events such as roadshows, travel fairs and campaigns as CAG, KAC and BMC collaborate to help grow and sustain the Singapore–Busan route.

Busan had been identified by OAG – a leading provider of digital flight information, intelligence and analytics – as the top unserved market for Changi Airport, with an estimated indirect two-way traffic exceeding 75,000 passenger movements annually.

Lim Ching Kiat, managing director, air hub development of Changi Airport Group, said: “For many years, connectivity between Singapore and South Korea has been limited to Seoul with around 60 weekly services. As Changi Airport is the gateway to South-east Asia and given the increasing travel demand over the years between Singapore and Busan, we are pleased to welcome the opening of this new route which will offer greater convenience for travellers between the two cities.”

Almost all visa applicants to the US need to submit social media information

Nearly all visa applicants to the US are now required to submit any information about social media accounts they have used in the past five years under a State Department policy, the Associated Press reported.

Under the newly adopted regulations that started on Friday, the US government will through such account information gain access to photos, locations, dates of birth, dates of milestones and other personal data commonly shared on social media.

Almost all visa applicants to the US need to submit social media information

The wider application of the Trump administration policy to request social media accounts – which was proposed in March 2018 – is estimated to affect 14.7 million people annually.

Only certain diplomatic and official visa applicants will be exempt from the stringent new measures, but people travelling to the US to work or to study will have to hand over their information, according to BBC.

“We already request certain contact information, travel history, family member information, and previous addresses from all visa applicants,” the State Department said in a statement. “We are constantly working to find mechanisms to improve our screening processes to protect U.S. citizens, while supporting legitimate travel to the US.”

Anyone who lies about their social media use could face serious immigration consequences, according to media reports.

IATA has downgraded its 2019 outlook for the global air transport industry to a US$28 billion profit, from US$35.5 billion forecast in December 2018, in the face of rising fuel prices and a weakening of world trade.

The association also restated its 2018 net post-tax profits, estimated at US$30 billion.

In 2019 overall costs are expected to grow by 7.4%, outpacing a 6.5% rise in revenues. As a result, net margins are expected to be squeezed to 3.2% (from 3.7% in 2018). Profit per passenger will similarly decline to US$6.1 (from US$6.9 in 2018).

Costs rising across the board; regional differences significant

“This year will be the 10th consecutive year in the black for the airline industry. But margins are being squeezed by rising costs right across the board – including labor, fuel and infrastructure. Stiff competition among airlines keeps yields from rising. Weakening of global trade is likely to continue as the US-China trade war intensifies,” said Alexandre de Juniac, IATA’s director general and CEO.

“Airlines will still turn a profit this year, but there is no easy money to be made.”

Moreover, the job of spreading financial resilience throughout the industry is only half complete with a major gap in profitability between the performance of airlines in North America, Europe and Asia-Pacific and the performance of those in Africa, Latin America and the Middle East.

“The good news is that airlines have broken the boom-and-bust cycle. A downturn in the trading environment no longer plunges the industry into a deep crisis. But under current circumstances, the great achievement of the industry – creating value for investors with normal levels of profitability is at risk,” said de Juniac.

Costs

The high price of fuel from 2018 (US$71.6/barrel Brent) will continue in 2019 with an average cost of US$70.00/barrel Brent expected. This is 27.5% higher than the US$54.9/barrel Brent in 2017. IATA says fuel costs will account for 25% of operating costs (up from 23.5% in 2018).

Non-fuel unit costs are expected to rise to 39.5 cents per available tonne kilometre from 39.2 cents, because of higher labor, infrastructure and other costs.

Overall expenses are expected to rise 7.4% to US$822 billion.

Overall revenues are not keeping pace with the rise in costs. For 2019, total revenues of US$865 billion are expected (+6.5% on 2018).

Passenger demand

IATA expects passenger demand to strengthen with global GDP growth expected to remain relatively strong at 2.7%, albeit slower than in 2018 (3.1%). Governments and central banks have responded to slower economic growth with more supportive policies, which is providing an offset to trade weakness.

But economic growth and household incomes will still grow more slowly, so total passenger demand, measured in revenue passenger kilometres, is expected to grow by 5.0% (down from 7.4% in 2018). Airlines have responded to the slower growth environment by trimming capacity expansion to 4.7% (ASKs).

Total passenger numbers are expected to rise to 4.6 billion (up from 4.4 billion in 2018).

Passenger yields are expected to remain flat in 2019 after a 2.1% fall in 2018.

Risk factors

Downside risks are significant. Political instability and the potential for conflict never bodes well for air travel. Even more critical is the proliferation of protectionist measures and the escalation of trade wars.

As the US-China trade war intensifies, the immediate risks to an already beleaguered air cargo industry increase. And, while passenger traffic demand is holding up, the impact of worsening trade relations could spillover and dampen demand.

“Aviation needs borders that are open to people and to trade. Nobody wins from trade wars, protectionist policies or isolationist agendas. But everybody benefits from growing connectivity. A more inclusive globalisation must be the way forward,” said de Juniac.

Regional roundup

All regions are expecting a reduction in profitability with the exception of North America and Latin America.

North American carriers will deliver the strongest financial performance with a US$15 billion post tax profit (up from US$14.5 billion in 2018). That represents a net profit of US$14.77 per passenger, which is a marked improvement from just seven years earlier (US$2.3 in 2012). Net margins, forecast at 5.5%, are down from 2018 levels owing to higher than expected fuel costs and slowing growth. The limited downside in this region has been underpinned by consolidation, helping to sustain load factors (passenger + cargo) above 65%, and ancillaries, which limit the impact of higher fuel costs, keeping breakeven load factors to 59.5%.

European airlines will deliver a net profit of US$8.1 billion (down from US$9.4 billion in 2018). That represents a net profit per passenger of US$6.75 and a net margin of 3.7% – both are the second strongest industry results, but below what North American carriers earn. Breakeven load factors are the highest at 70.2%, caused by low yields due to the highly competitive open aviation area, high regulatory costs, and inefficient infrastructure. In 2019, for example, en-route air traffic management delays doubled to 19.1 million minutes. Europe also is one of the more exposed regions to weak international trade and this has damaged prospects this year.

Asia-Pacific airlines will deliver a net profit of US$6.0 billion (down from US$7.7 billion in 2018). That represents a net profit per passenger of US$3.51 and a net margin of 2.3%. The region is showing very diverse performance.

Middle Eastern airlines will deliver a combined net loss of US$1.1 billion (slightly worse than the US$1.0 billion loss in 2018). That equates to a US$5 loss per passenger and a negative net margin (-1.9%). The region has faced substantial challenges in recent years, both to the business environment and to business models. Airlines there are going through a process of adjustment and announced schedules point to a substantial slowdown in capacity growth in 2019. Performance is now improving but the worsening in the business environment is expected to prolong losses in 2019.

Latin American airlines will deliver a net profit of US$200 million. This reflects a moderate improvement from the US$500 million loss in 2018, as the recovery of the Brazilian economy is offsetting higher oil prices. With a US$0.50 profit per passenger, the region’s net margin is expected to be a thin 0.4%.

African airlines will deliver a US$100 million loss (unchanged from 2018), continuing a weak trend into its fourth year. Each passenger carried is expected to cost the carriers US$1.54, leading to a -1.0% net margin. Breakeven load factors are relatively low, as yields are a little higher than average and costs are lower. However, few airlines in the region are able to achieve adequate load factors, which averaged the lowest globally at 60.7% in 2018. Overall, industry performance is improving, but only slowly.

THAI Smile Airways is expected to join the Star Alliance network as connecting partner by the end of this year, joining Juneyao Airlines that entered in 2017.

Connecting partners allow Star Alliance to close network gaps that may exist of a regional basis. THAI Smile Airways will add 11 new destinations to the Star Alliance network, which already comprises over 1,300 airports in 194 countries.

THAI Smile Airways in Chiang Rai

The Bangkok-based airline has begun to implement the necessary technology and commercial links which will allow THAI Smile to begin serving Star Alliance connecting passengers in 2020. Once that is complete, the airline will be able to offer privileges to qualifying Star Alliance Gold Status passengers, including priority check-in, Thai Smile lounge access and priority baggage delivery.

The programme was established by Star Alliance in June 2016 to complement its membership model.

In contrast to full membership in the alliance, which requires the building of commercial ties with all full members, the more regional connecting partner scope calls for commercial relationships with a minimum of three carriers only.

Customers travelling on an itinerary which includes a transfer between a Star Alliance member airline and a connecting partner will be offered standard Alliance benefits such as passenger and baggage through check-in. In addition, customers who have achieved Star Alliance Gold Status in their frequent flyer programme will enjoy premium customer benefits.

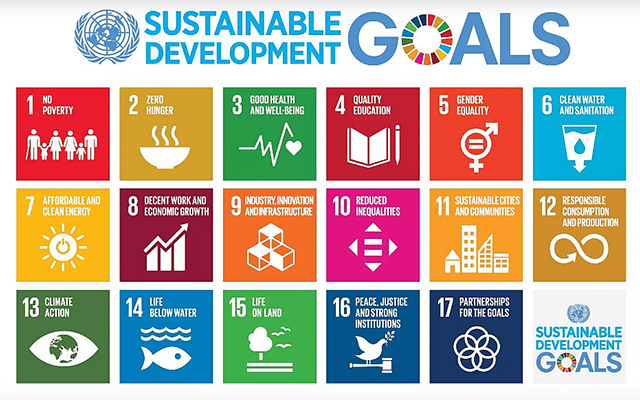

Ground Asia has integrated 14 out of 17 sustainable development goals (SDG) into its 50 student travel and community engagement experiences in six Asian countries.

For example, the Rural Business Development Study trip in Cambodia supports goals 1, 8, 9, 10, 11: poverty alleviation; decent work and economic growth; industry innovation and infrastructure; reduced inequalities; and sustainable cities and communities.

UN Sustainable Development Goals

The Physiotherapy in Vietnam student journey supports goal 3: good health and well-being.

Mangrove Protection in Bali supports goals 11 to 15: sustainable cities and communities; responsible consumption and production; climate action; life below water; life on land; and so on.

In the new SDG affiliation, Ground Asia also identifies learning outcomes that students can expect from each trip.

Lauren Groves, general manager of the Thailand-based company, said: “The UN SDGs are not going to be achieved without the efforts of many individuals, companies, NGOs, and civic organisations around the world. So, as Ground Asia is dedicated to the triple bottom line, we are doing what makes sense and committing to a wider, more noble set of goals through educational travel.”

Royal Caribbean International’s Spectrum of the Seas has arrived in Hong Kong, attended by over 600 invited government officials, industry stakeholders and loyal guests.

Officiating guest Edward Yau Tang-wah, secretary for commerce and economic development said the Hong Kong government has been joining hands with the Hong Kong Tourism Board and the trade in promoting the development of cruise tourism in Hong Kong.

Spectrum of the Seas' arrival in Hong Kong

1 of 2

Spectrum of the Seas

Royal Caribbean Cruises' Michael Bayley

With accommodation for 5,622 guests and 2,147 staterooms, Spectrum of the Seas set off on its maiden voyage to Asia from Europe just a month ago. Highlights of the new cruise include a first-at-sea virtual reality, bungee trampoline experience, suites-only area, Ultimate Family Suite and a Sichuan specialty restaurant.

Guests can also now utilise the new Royal app to plan and manage their cruise holiday while on board. The app enables access to the guest’s suite, controls amenities inside the suite, and allows guests to make specialty and dining reservations, reserve shore excursions and shows, access their bill in real-time, and save daily activities to their calendar.

From December 2019 to January 2020, Spectrum of the Seas will offer six cruises from Hong Kong. The seven-night Japan & Philippines Cruise departing on December 22, 2019 and January 2, 2020 will visit Ilocos in the Philippine where guests can enjoy the beaches and explore historic Vigan City, home to Spanish baroque colonial architecture.

There is also the four-night Best of Chan May Cruise, departing on December 18 and 29, 2019.

From November 2020 to January 2021, Spectrum of the Seas will return to Hong Kong for nine homeport sailings. In addition, there will be two special Olympic-themed sailings in 2020 in celebration of the great sports event. Departing from Shanghai on July 25 and August 2 respectively, Spectrum of the Seas will bring guests to Tokyo during the Summer Olympics and stay overnight to indulge in the exciting Olympic sports enthusiasm.

From left: China Eastern Airlines' Dong Bo, former SkyTeam Alliance board chair Michael Wisbrun, SkyTeam's Kristin Colvile and Korean Air's Walter Cho

SkyTeam, the global airline alliance, has announced Walter Cho, chairman and CEO of Korean Air, as the new chairperson of its alliance board.

The appointment was endorsed last week at a meeting of the SkyTeam Alliance Board, which comprise CEOs of the 19 member airlines and oversees SkyTeam’s global strategy.

As a founding member, Korean Air has been instrumental in shaping SkyTeam over the last 20 years.

From left: China Eastern Airlines’ Dong Bo, former SkyTeam Alliance board chair Michael Wisbrun, SkyTeam’s Kristin Colvile and Korean Air’s Walter Cho

Walter Cho will replace the chairperson of the alliance board, Michael Wisbrun, who has held the position for more than three years.

Apart from steering a fleet modernisation programme and negotiating a Trans-Pacific joint venture with Delta Airlines, he is also recognised for his expertise and experience in the IT field. Cho successfully implemented key IT initiatives of the airline, including the advanced enterprise resource planning, the new passenger service and the next-generation cargo system (iCargo).

He also made a pioneering decision to migrate Korean Air’s IT system to Amazon Web Services cloud.

SkyTeam has also introduced an executive board to its governance structure.

Earlier this month, Dong Bo, chief marketing officer, China Eastern Airlines was appointed the chairperson of this board.

Created to support SkyTeam’s focus on customer experience enabled by technology, the executive board is made up of senior business leaders from each of the member airlines who will be actively involved in implementing the alliance’s strategy.

Since joining China Eastern Airlines in 1997, Dong Bo has been deputy general manager of the Human Resources department, general manager of the cabin crew service department, secretary (then general manager) of ground handling department, chief service officer, chief marketing officer and general manager of marketing & sales committee.

“SkyTeam is entering the next generation of its life, these two appointments reflect our members’ commitment and broader engagement in creating the leading alliance of the future, with a significant focus on digitally connecting airlines to create an effortless and seamless customer experience, enabled by proprietary technology,” said Kristin Colvile, SkyTeam’s CEO and managing director.

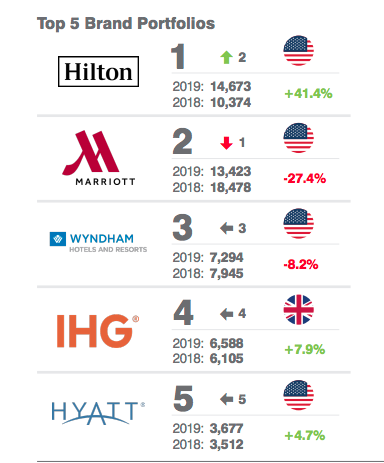

While Hilton clinched the lead in terms of value of top performing brands in a recent ranking, it is also playing catch up with Marriott in the luxury space.

According to Brand Finance’s latest hotel sector report released in May, the value of Hilton brands that made the top 50 ranking this year was at US$14.7 billion – over US$1 billion ahead of Marriott’s US$13.4 billion portfolio. Hilton achieved overall brand value growth of 41 per cent, while Marriott saw a 27 per cent decrease, making way for Hilton in the top spot. Hilton has six brands in the top 50, compared to Marriott’s 13.

Brand Finance's Hotels 50 2019 report

1 of 3

Most valuable brand portfolios

Top brands by value

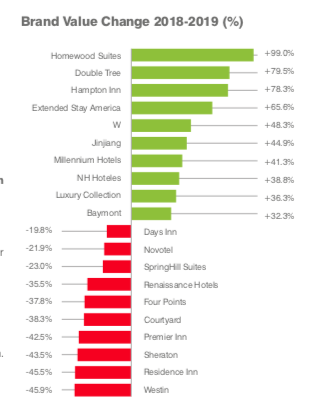

Brand value change

Brand recognition and innovation are driving Hilton’s performance, Daniel Welk, the group’s vice president, luxury and lifestyle, Asia Pacific, told TTG Asia on the sidelines of ILTM Asia Pacific.

“We’re not saying we’re the biggest hotel company in the world, just the most recognisable and trusted throughout the globe. It’s rankings like this that allow us to hang our hat on (that claim),” said Welk.

“We’re (akin to a) 100-year-old start-up. Everyone at Hilton believes that innovation is in our DNA. Today we are leading digital technology by (pioneering a) mobile app that allows room selection, digital key (and more).”

The Hilton Hotels & Resort flagship, already the most valuable brand on the ranking, this year extended its lead over Marriott, after growing 17 per cent in value to US$7.4 billion. This was largely driven by strong revenue increase over the last year, according to Brand Finance.

Moreover, the independent brand-valuation company found the top three fastest growing brands all coming from Hilton’s portfolio, led by Homewood Suites (brand value up 99 per cent to US$800 million), followed by Double Tree (up 79 per cent to US$2.1 billion) and Hampton (up 78 per cent to US$3.2 billion).

Hilton rules the roost in the report

On the other hand, Marriott is holding strong in luxury. Notably, the group’s only two brands in the top 10 growth ranking were both from the luxury category (W and Luxury Collection).

Travel agents polled at ILTM Asia Pacific said the giant’s luxury brands continue to score high on brand trust and recognition, despite Brand Finance partly attributing Marriott’s decline in brand value to a recent cyber security incident.

Buyer Vikram Kajaria of Makson Travels said: “Hilton’s Waldorf Astoria aside, Marriott’s luxury brands such as the Ritz-Carlton and St Regis are more trusted and recognised among high-end Indian travellers.”

Nevertheless, Hilton’s luxury portfolio is on a steady climb. Welk said “incubating new brands” is another way the group is working to stay ahead in luxury. After recent debuts, Hilton today counts four of its 17 brands in luxury and lifestyle.

Hilton recently debuted the Canopy brand before bringing it to Asia with an opening in Chengdu this year. It also introduced LXR late last year, a new soft brand of individual properties, each distinct from the other, but all carrying the promise of uncommon and personalised experiences.

Asia-Pacific represents an important region as the world’s two most valuable hotel groups pursue growth in the luxury sector.

“The whole centre of gravity in the hospitality world is moving to Asia-Pacific. Throughout the region, we have in excess of 20 luxury and lifestyle hotels in the pipeline. There are 24 hotels (in the region) across the three brands – Waldorf Astoria, Conrad and Canopy by Hilton,” Welk shared.

Rival Marriott is also making big investments in the Asia-Pacific luxury space. It announced last week that there will be 13 new luxury projects to open in 2019, a feat considering the size of the high-end sector, according to Bruce Ryde, vice president, luxury brand management, Asia Pacific.

Ryde added that the hotel giant is rolling out a “luxury countdown process”, an internal initiative that originated with a Ritz-Carlton, to all its luxury brands. “It’s where senior people and luxury resources descend on a hotel eight to 10 days out (from its opening) to envelop the team at the property with (passion) and brand speak. This is so we give the hotel the best possible start in the luxury space.”

New and upcoming luxury hotel openings the St Regis in Hong Kong, while the Ritz-Carlton is set to launch in Xi’an (China), Perth (Australia) and Pune (India).

Brand Finance also pointed out that Marriott’s recent announcement to enter the longer-stay market to take back share from Airbnb could drive its brand value back up in the coming year.

Aerial view of tourists from Russia and other countries on a basket boat tour of the Mangrove Palm forest in Cam Thanh village, Hoi An

It’s boom time for Russian arrivals in Asia-Pacific countries, which ForwardKeys attributes to a doubling in seat capacity on direct flights from Russia to select destinations in the region.

Direct flights from Russia to Asia-Pacific more than doubled as airlines increased their seat capacity substantially. Overall seat capacity was up 37.6%, with the highlights being a 124.8% increase in seats to Thailand and 153% to Vietnam.

Aerial view of tourists from Russia and other countries on a basket boat tour of the Mangrove Palm forest in Cam Thanh village, Hoi An

Total international arrivals in Asia-Pacific were up 3.8% from May 2018 to April 2019. However, Russia’s 54.5% increase meant Europe was the top growing origin continent, up 6.3%.

ForwardKeys notes the extent of Russia’s sharply renewed enthusiasm for Asia-Pacific after reviewing historical figures. The volume of arrivals rocketed towards the end of last summer, according to ForwardKeys’ data.

Growth in Russian leisure travellers (up 62.8%) dramatically outstripped business travel (up 27.5%) and they’re staying for 16 nights on average. In line with general trends towards shorter lead times, the Russians are booking fewer days in advance, 65.8 days, down from 78.1 days.

ForwardKeys vice president, insights, Olivier Ponti, said: “For the Asia-Pacific region, Russia is now the ninth top origin country – by share – outside of Asia-Pacific itself. It’s due to a combination of increased seat capacity on direct flights, high-profile political visits and astute marketing… as well as agile capacity meeting demand.”

")